The bond market reacted decisively to Donald Trump’s success in the U.S. presidential election. Ten-year treasury yields rose from 1.86% on November 8th to 2.37% on November 25th.

Trump’s promise to invest $550 billion in infrastructure over the next decade in conjunction with tax cuts are being interpreted by the market as inflationary. Tax cuts will most likely increase spending, which may drive inflationary pressures given that the U.S. is close to full employment. Higher levels of borrowing to finance infrastructure may also require higher interest rates.

Evolving expectations

The plans of President-elect Trump to “revive” the economy are still vague. This may be one reason why the bond market has not overreacted. Yields are back to where they were in December 2015 and are still way below December 2013 levels of 3%.

Furthermore, long term (10 year) inflation expectations remain benign with the most recent figures published by the Cleveland Federal Reserve at 1.75%, only slightly higher than today’s levels of 1.6%. But has the bond market become too complacent?

Chart 1: US 10 Y Bond Yields and Inflation

Building bridges

During the election campaign, Trump’s advisers said the infrastructure plan involves the private sector putting up 20% of the money, with most of the remainder financed via tax credits. The challenge, of course, is that a lot of infrastructure doesn’t suit privately funded capital in terms of being able to extract sufficient returns. This remains a major weakness in his plan and may well be why the bond market hasn’t moved that much.

The federal government could raise long term debt to finance the investment, however, fiscal hawks would no doubt oppose such a plan. Clearly, borrowing large amounts of money in the hope that tax contributions will rise to pay down the debt is a gamble. Given that there remains a significant demand for high quality assets by investors across global capital markets, it seems unlikely that interest rates would rise dramatically — but there would most likely be some effect.

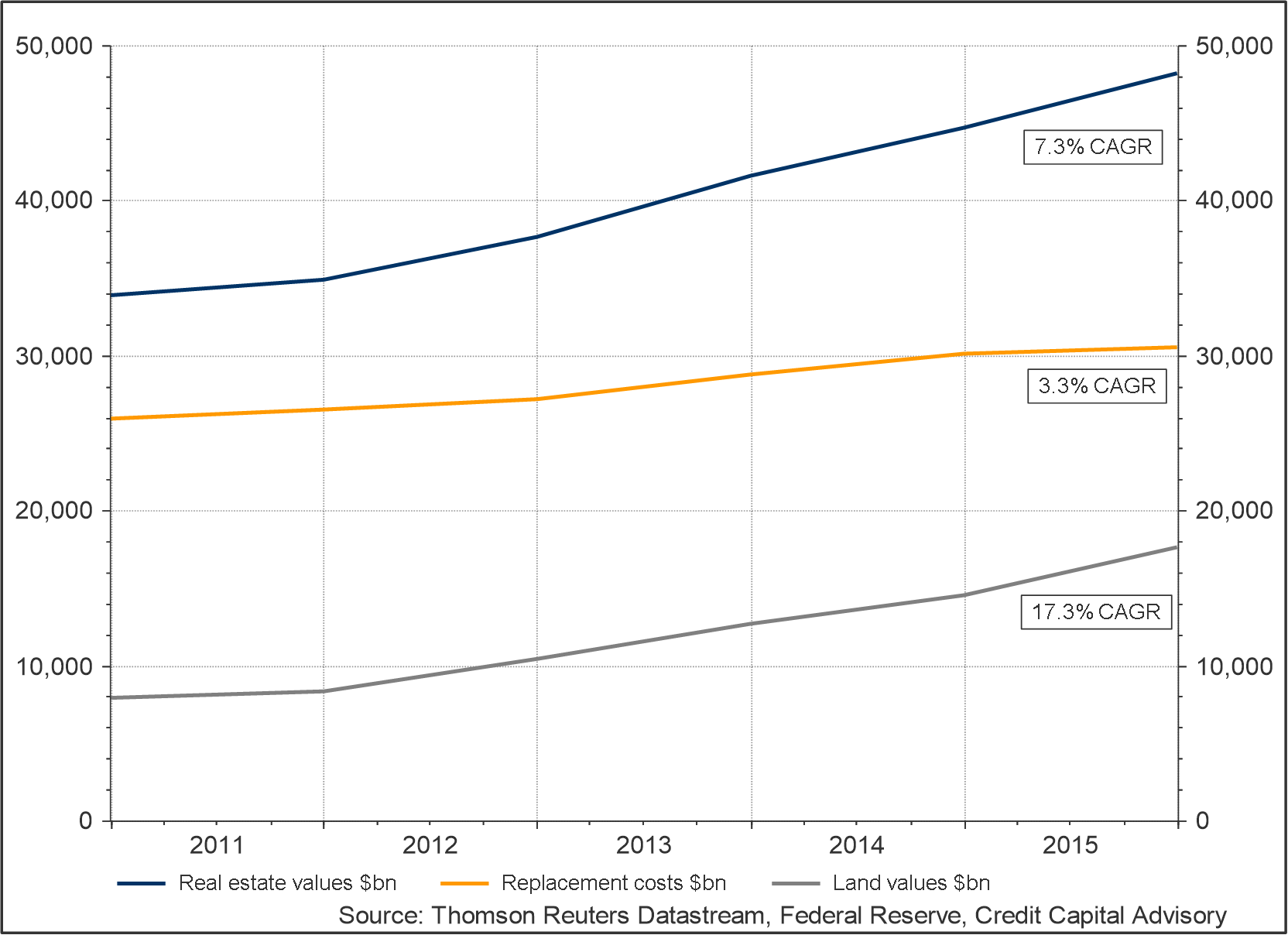

Trump could instead promote widely used infrastructure financing mechanisms for his $550 billion investment program such as land value capture. This is where the municipality or state captures the uplift in land values due to the infrastructure investment. Bond holders who provide the initial capital are then paid back via the cash flows generated from rising land values.

An analysis of the flow of funds data highlights that land values have increased at an incredible compound annual growth rate of 17% between 2010 and 2015 compared to just 7% for real estate. Between 2014 and 2015, land values increased by $3.1 trillion which is computed as the total value of real estate minus its replacement costs. Being able to capture just 18% of one year’s rise in land values would completely finance Trump’s plan with far less impact on interest rates.

Chart 2: Growth in US land values 2010 – 2015

Rise or fall?

If the president-elect is able to draft a realistic financing mechanism for his infrastructure plan, bond investors will be watching the labor market for signs of wage inflation. Unemployment hit 4.6% in November and if the president-elect goes ahead and expels three million illegal immigrants, the rate may well fall further as the Bureau of Labor Statistics notes that illegal workers are probably captured in the labor force survey.

However, the localized nature of infrastructure, in addition to the time lags in kicking off projects, suggests that any inflationary effect is some years away. Moreover, the current depressed labor force participation rate at just under 63%, could revert to the 66% level it was between 1989 and 2008 as a result of training and incentives.

Chart 3 shows another reason why the bond market is sanguine about inflation, with the blue line demonstrating a very strong trade-weighted dollar, which will depress import prices. Furthermore, the red line, which shows commodity prices, remains subdued despite the recent increase in the price of oil, as does the gray line highlighting China’s producer price index. To what extent these deflationary factors will be cancelled out by the increase in domestic final demand as a result of tax cuts remains to be seen. The link between the producer price index and CPI is unsurprisingly close as shown in green and orange.

Chart 3: U.S. Inflationary indicators

Prices & protectionism

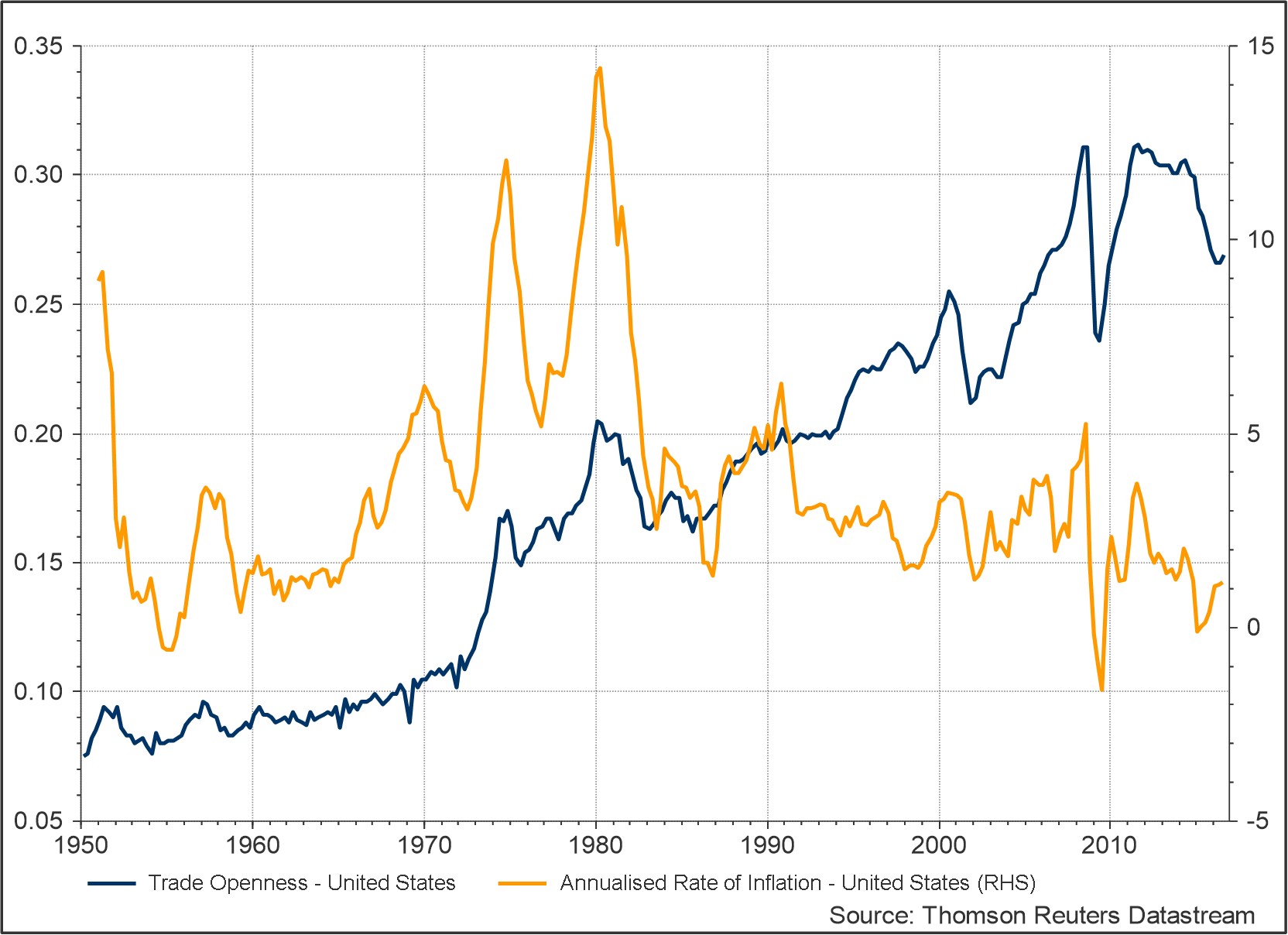

However, the bond market needs to be extremely wary of any shift towards protectionism. Trump’s plan to tax firms 35% for selling their products back into the United States after off-shoring manufacturing will almost certainly drive up inflation, given current levels of unemployment. Long run data from the U.K. suggests that the more open the economy, the less responsive wages are to falling unemployment, due to greater competition.

Chart 4 shows the relationship between inflation and trade openness between 1950 and 2015 for the U.S. The relationship is clear that any move towards protectionism is likely to drive inflation. Should the trade openness ratio fall to 0.2, then bond investors are likely to start seeing red.

Chart 4: U.S. Trade openness and inflation