Concerns about persistent underinvestment in the U.S. economy resulting from the financial crisis are overblown. The underlying issue is that the lack of a robust anti-trust framework has made it too easy for dominant firms to increase profits. Without sufficient competition, the incentives to increase the rate of productivity have fallen. Although this has been and still is a boon for equities, investors should note that the current economic system is rapidly falling out of favour with voters across the developed world.

Is the U.S. economy really underperforming?

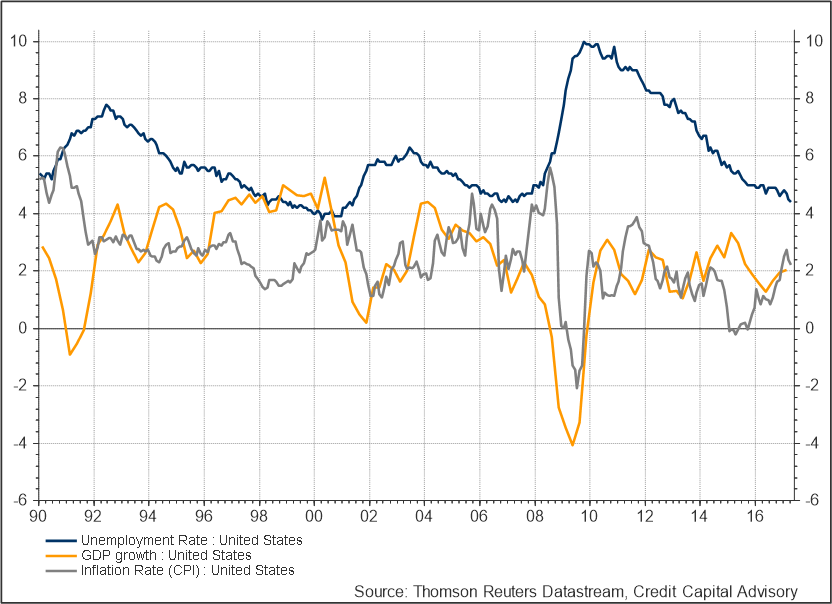

The data for the U.S. economy can be made to fit numerous hypotheses about its performance. Chart 1 suggests that the economy is in pretty good shape. The unemployment rate remains close to record lows, although the participation rate at 63% is somewhat down from pre-crisis levels of 66%. Inflation is stabilizing around 2% with GDP growth around 2%, slightly down from a pre-crisis average of 2.5% (2001-2007).

Chart 1: U.S. Unemployment, inflation and GDP

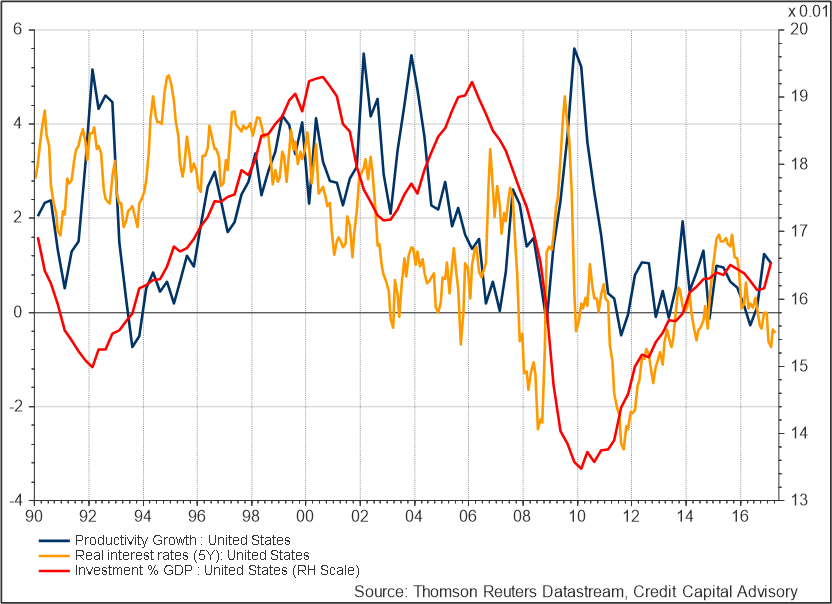

However, Chart 2, which shows productivity, investment and real interest rates, suggests something is amiss. Investment levels, although above post-crisis levels, appear to have plateaued at around 16% of GDP compared with 18% prior to the boom, despite five-year real interest rates remaining below zero. Critically, productivity levels have struggled to rise above 1%. As productivity growth is the key determinant of real income levels and investment is key to productivity growth, the state of these indicators has raised numerous concerns amongst economists, particularly given that the cost of borrowing remains so low.

Chart 2: Productivity, real interest rates and investment

Diverging explanations

These contradictory signals have led to the development of a number of theories. Larry Summers has argued that the economy has entered into a period of secular stagnation, with lower demand acting as a barrier to lower investment. If saving exceeds investment, it can lead to lower levels of aggregate demand and stunted growth. However, the U.S. economy continues to add jobs at a reasonable rate and overall output is not too far off average pre-crisis levels. Furthermore, it is not clear whether comparing to pre-crisis levels is a sensible idea, given that there is evidence that output levels during the credit boom may not have been sustainable.

Ken Rogoff has argued that the debt overhang from the credit boom has been a major challenge for growth. Although the consumer debt to income ratio fell from record highs in 2007 of 133%, it has been pretty stable at levels of 104% for more than two years. Moreover, as I argued here, leverage ratios in the U.S. economy are now in fact increasing. Finally, Robert Gordon has suggested rather gloomily that the age of innovation is over, and that we just have to get used to this. However, this does not tally with expectation that automation will make redundant aspects of many jobs.

Which data?

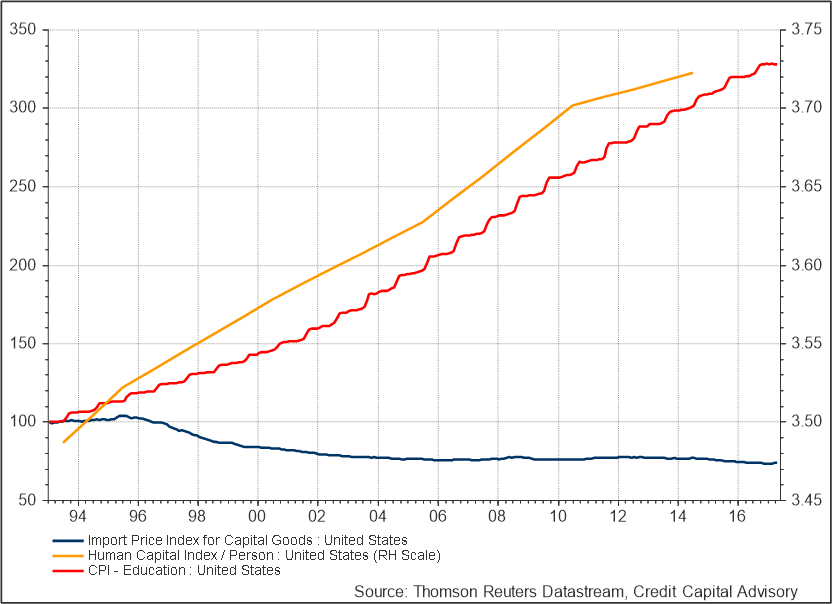

One important issue that Summers raises is that the cost of investment goods has been falling. Hence it should not be surprising that investment as a percentage of GDP should have fallen too. However, it is not clear why this is something to worry about. If investment goods are falling, this is a sign that productivity in the manufacture of these goods is rising. Furthermore, capital goods play an increasingly diminishing role in raising productivity. Elevated levels of human capital are far more important. Chart 3 shows the rising levels of human capital as the cost of investment goods falls. The chart also shows that the cost of education has continued to rise unabated.

Chart 3: Human capital, cost of education and price of investment goods

Low interest rate paradigm

One impact of the shift away from the acquisition of investment goods to acquiring human capital is that the latter has almost no relationship to interest rates. Rising demand for capital goods would typically lead to rising demand for loans to acquire those goods, hence interest rates typically rose as economies came out of recession. But this is far less likely to happen now. As argued here, as long as existing global trade arrangements remain in place, interest rates are unlikely to shoot up.

However, policy makers still need to get to grips with this paradigm shift, particularly given that low rates will also have a tendency to drive up house prices and encourage speculative investment into existing assets. Housing markets are notoriously inefficient and prone to boom and bust. But jacking up interest rates is unlikely to curb these excesses without inflicting significant damage on the economy.

Although the above data is able to explain lower levels of interest rates and lower investment levels, it does not explain why productivity has fallen.

Path of least resistance

Corporate managers unsurprisingly take the easiest path to increase profits, which may or may not require an increase in productivity. If there are more immediate sources of profit growth, then there is little incentive to improve productivity.

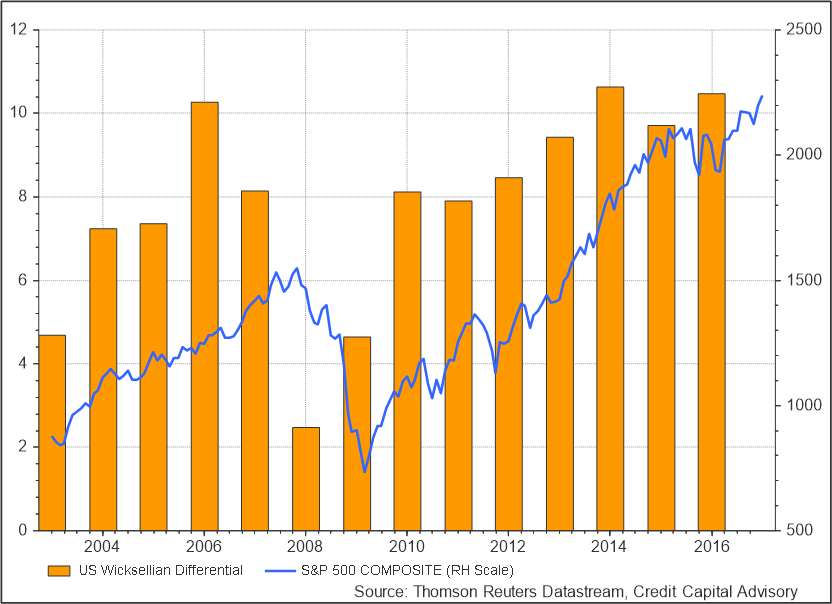

An analysis of the Wicksellian Differential – the return on capital minus the cost of capital – demonstrates that corporations have been able to increase profits to record levels. The current lower levels of productivity suggest that managers are relying on other factors to boost profits such as market power and cheap credit. Data from The Economist suggest that the world is becoming increasingly less competitive. If managers are able to hit their profit targets through leveraging market power, then there is less incentive to drive productivity growth, which is much harder to achieve.

Chart 4: U.S. Wicksellian Differential vs S&P 500

Although equity investors have been enjoying the fruits of robust profit growth, the economic system that is generating these profits is coming under increasing scrutiny. Investors would do well to manage their portfolios using dynamic asset allocation strategies, as the outlook for equities will not always be positive — particularly if the government decides that increased intervention is necessary to promote greater competition.